China’s $17 Trillion Debt Mountain Isn’t as Scary as It Looks

by and- The country’s top firms are cleaning up their balance sheets

- Deutsche Asset is bullish on large-cap Chinese stocks

China Inc. Healthy in Spite of Debt

There’s been no shortage of bad news when it comes to China’s massive debt pile, from turbulence in the corporate bond market to last month’s sovereign rating downgrade by Moody’s Investors Service.

But look beyond the negative headlines, and one encouraging fact stands out: China’s biggest companies are healthier than they’ve been in years.

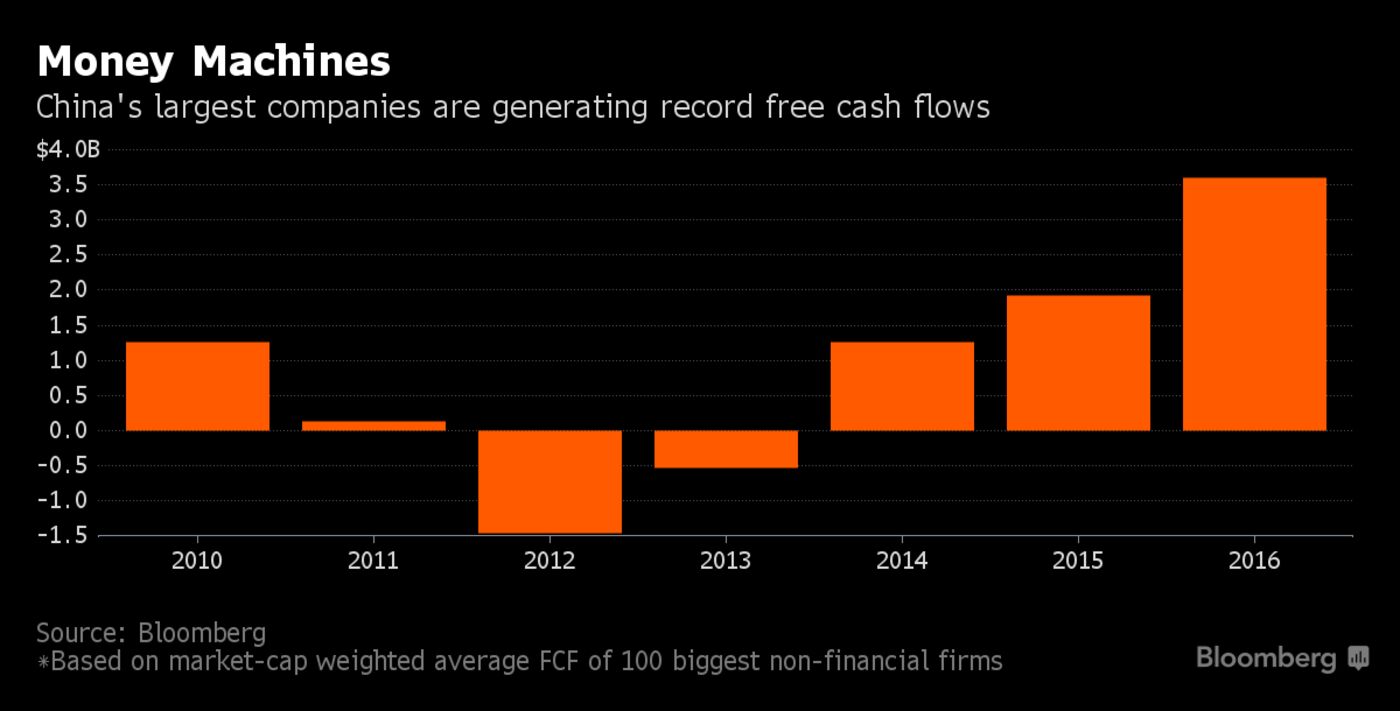

Thanks to a combination of economic stimulus and state-owned enterprise reform, debt-to-equity ratios at China’s largest non-financial firms have dropped to the lowest levels since 2010. Gauges of profitability and interest payment capacity are the strongest in at least five years, while free cash flows have never been bigger.

The improvements could help ease fears of a looming financial crisis in the world’s second-largest economy, even though smaller Chinese companies have made less progress so far. Deutsche Asset Management, which oversees about $800 billion, says stronger balance sheets support a bullish outlook for China’s stock market after the Shanghai Composite Index trailed all of its Asian peers this year.

“We’re quite positive on Chinese stocks generally, especially larger caps,’’ said Sean Taylor, chief investment officer for Asia Pacific at Deutsche Asset in Hong Kong. “Profits are rising and they’re not taking on as much debt.”

The prevailing mood in Chinese markets is much more downbeat. Even before Moody’s cut the government’s credit rating on May 24, fund managers surveyed by Bank of America Corp. cited tightening credit conditions in China as the top “tail risk” for global financial markets. A government crackdown on leverage helped push company bond yields to a two-year high last month, rekindling anxiety over a corporate debt load that swelled to an estimated $17 trillion last year, or 156 percent of gross domestic product.

Despite those concerns, vital signs at the country’s largest listed companies are getting stronger. The market capitalization-weighted average debt-to-equity ratio at China’s 100 biggest non-financial businesses dropped to 68 percent at the end of last year from 72 percent in 2015, according to data compiled by Bloomberg. Profit margins and interest coverage ratios also improved, while free cash flows for the group swelled to a record $93 billion.

Stronger corporate credit metrics help explain why there’s been little sign of a pickup in defaults as borrowing costs rise, according to Goldman Sachs Group Inc.

“We see plenty of room for policies to tighten without resulting in widespread corporate distress,” Kenneth Ho, a Hong Kong-based analyst at Goldman Sachs, wrote in a research report dated May 31.

Accelerating economic growth has made it easier for big companies to repair their balance sheets. China’s GDP increased 6.9 percent in the first quarter from a year earlier -- the first back-to-back acceleration in seven years -- as investment, retail sales and factory output all strengthened. Raw-materials producers got an added boost from government-led efforts to reduce oversupply.

The capacity cuts are part of President Xi Jinping’s plan to revamp the country’s state-owned enterprises, which dominate the ranks of big mainland-listed stocks. Chinese policy makers see higher SOE profitability as a key element of the nation’s shift toward a more sustainable economic growth model.

“Some of the industrial companies remain heavily in debt, but the situation is improving,” said Jing Ulrich, vice chairman of Asia Pacific at JPMorgan Chase & Co. in Hong Kong.

Temporary Boost

To be sure, the financial metrics compiled by Bloomberg exclude unlisted borrowers and heavily-indebted local governments. Skeptics say even the improvements at big public companies are temporary -- the result of economic pump-priming before a politically-sensitive leadership reshuffle in the ruling Communist Party toward the end of this year. The economy’s strong start to 2017 has already shown signs of leveling off, with a private gauge of manufacturing signaling a contraction in May.

Raw-materials producers are particularly vulnerable amid a pullback in commodities prices, according to Xia Le, a Hong Kong-based economist at Banco Bilbao Vizcaya Argentaria SA.

And yet, shares of China’s biggest companies are rising. The CSI 300 Index of large-cap stocks has climbed 5.5 percent this year, versus a 0.1 percent decline in the Shanghai Composite and a 10 percent drop in the smaller-company ChiNext index.

While government intervention has probably fueled some of the large-cap rally, AIA Group Ltd.’s Mark Konyn sees scope for optimism.

Big businesses are “key heavyweights in the economy,” said Konyn, group chief investment officer at the Hong Kong-based insurer. “They are a good indicator of what’s going on.”

No comments:

Post a Comment