ROILO GOLEZ, Philippine National Security Adviser (2001-2004). The world and the Philippines as Roilo Golez sees it. With focus on national security, geopolitics, geo-security, economics, science and government.

Monday, January 30, 2017

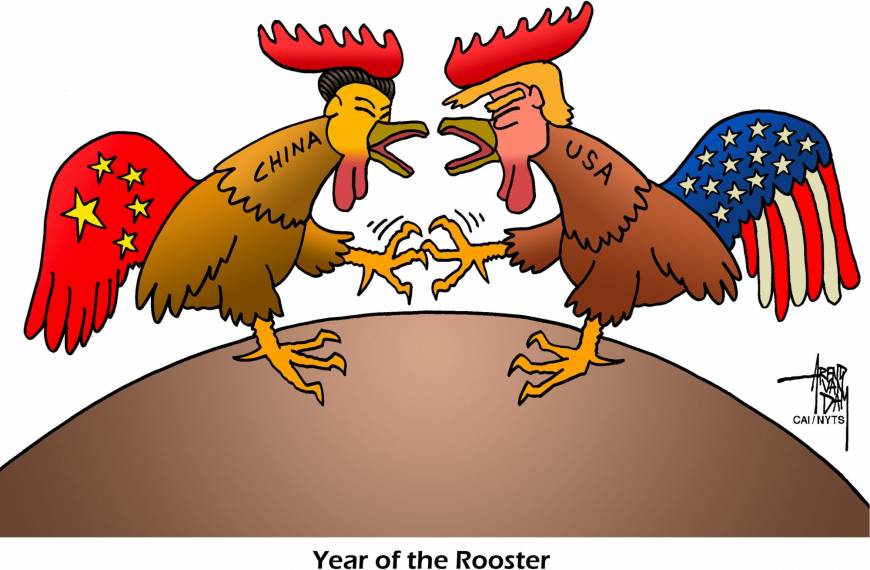

Golez: This is both an economic and security issue. Much of China's rise, and the resultant security threat it poses in the Asia Pacific are and beyond, is because of its economic rise that has now slowed down

Golez: This is both an economic and security issue. Much of China's rise, and the resultant security threat it poses in the Asia Pacific are and beyond, is because of its economic rise that has now slowed down:

"...the era of China’s growth by exporting is over because just about all of the manufacturing jobs that could be moved from the West to China and other developing countries have left. In the late 1990s, 17 percent of U.S. gross domestic product came from manufacturing. In 2009, the share fell to 12 percent and then leveled off. Chinese exports used to rise 20 percent to 30 percent per year but now are falling.

"Chinese infrastructure spending, used to offset waning exports, has spawned huge excess capacity, ghost cities and debt, which together leaped from 164 percent of GDP in 2008 to 247 percent in 2015, based on the latest data available. The planned shift to consumer spending and services is behind schedule and troubled. Sizable increases in minimum wages, designed to promote household spending, have displaced low-end manufacturing to cheaper locales such as Vietnam and Pakistan. The bubbly Chinese real estate sector appears to have peaked. China’s economic growth is slipping and the 6.7 percent official GDP number for 2016 probably is double the true number.

"The era of China’s growth by exporting is over because just about all of the manufacturing jobs that could be moved from the West to China and other developing countries have left. In the late 1990s, 17 percent of U.S. gross domestic product came from manufacturing. In 2009, the share fell to 12 percent and then leveled off. Chinese exports used to rise 20 percent to 30 percent per year but now are falling.

"Chinese infrastructure spending, used to offset waning exports, has spawned huge excess capacity, ghost cities and debt, which together leaped from 164 percent of GDP in 2008 to 247 percent in 2015, based on the latest data available. The planned shift to consumer spending and services is behind schedule and troubled. Sizable increases in minimum wages, designed to promote household spending, have displaced low-end manufacturing to cheaper locales such as Vietnam and Pakistan. The bubbly Chinese real estate sector appears to have peaked. China’s economic growth is slipping and the 6.7 percent official GDP number for 2016 probably is double the true number.

"Trump’s hyperbolic call for a 45 percent tariff on Chinese imports is, no doubt, the opening gambit from a man who considers himself the world’s best negotiator. Whether his business successes transfer to the international arena remains uncertain, but he’s well aware that, in the present world of excess capacity and ample labor, it’s the buyer — the U.S. — that has the upper hand, not China, the seller.

"Xi may be right that no one wins a trade war, but the U.S. will probably lose less than China. That will boost the dollar further, as will its haven status and the almost universal attempts by nations to devalue their currencies. As a result, earnings at American exporters will suffer as the dollar gets stronger. Conversely, domestically oriented U.S. companies will be better off, especially in those service industries that are relatively immune to imports."

NEW YORK – One clear takeaway from Chinese President Xi Jinping’s Jan. 17 speech at the World Economic Forum in Davis was that U.S. President Donald Trump has him on the defensive.

Xi delivered a minor surprise by passionately backing free trade in a rebuke to the protectionist platform that helped Trump get elected. “No one will emerge as a winner in a trade war,” Xi said. What he forgot to say is that those conflicts are never officially declared, and China has been in one for years.

It’s one thing for China to use its cheap and disciplined labor force to grow rapidly through exports, most of which directly and indirectly end up in North America and Europe. It’s another to dump excess steel, aluminum and other products on world markets.

The pressure is on. The era of China’s growth by exporting is over because just about all of the manufacturing jobs that could be moved from the West to China and other developing countries have left. In the late 1990s, 17 percent of U.S. gross domestic product came from manufacturing. In 2009, the share fell to 12 percent and then leveled off. Chinese exports used to rise 20 percent to 30 percent per year but now are falling.

Chinese infrastructure spending, used to offset waning exports, has spawned huge excess capacity, ghost cities and debt, which together leaped from 164 percent of GDP in 2008 to 247 percent in 2015, based on the latest data available. The planned shift to consumer spending and services is behind schedule and troubled. Sizable increases in minimum wages, designed to promote household spending, have displaced low-end manufacturing to cheaper locales such as Vietnam and Pakistan. The bubbly Chinese real estate sector appears to have peaked. China’s economic growth is slipping and the 6.7 percent official GDP number for 2016 probably is double the true number.

Xi’s response involves a competitive devaluation of the yuan, a normal protectionist measure aimed at encouraging exports and discouraging imports. But to limit capital flight and curtail foreign criticism, China’s central bank surreptitiously alternates between emphasizing the currency’s link to the dollar and to a trade-weighted basket. China’s foreign currency reserves have been cut to $3 trillion from as much as $4 trillion in June 2014.

Despite Xi’s pleas at Davos, free trade is rare, and only occurs when a global power uses it to its advantage. The United Kingdom did so in the 19th century to secure raw materials for its rapidly industrializing economy and markets for its output.

Post-World War II, the United States used free trade to promote recovery in Western Europe and Japan. That was cheaper than garrisoning more American troops around the world to contain communism.

Most Americans accepted that strategy and tolerated rapid growth in China — until globalization moved so many manufacturing jobs there that real incomes declined for most Americans, starting over a decade ago. The deleveraging of the excess debt accumulated in the 1980s and 1990s, contributing to sluggish economic growth and depressed wages in the West. Furthermore, American business cut labor costs to promote profits in the absence of significant revenue growth.

Trump’s hyperbolic call for a 45 percent tariff on Chinese imports is, no doubt, the opening gambit from a man who considers himself the world’s best negotiator. Whether his business successes transfer to the international arena remains uncertain, but he’s well aware that, in the present world of excess capacity and ample labor, it’s the buyer — the U.S. — that has the upper hand, not China, the seller.

Xi may be right that no one wins a trade war, but the U.S. will probably lose less than China. That will boost the dollar further, as will its haven status and the almost universal attempts by nations to devalue their currencies. As a result, earnings at American exporters will suffer as the dollar gets stronger. Conversely, domestically oriented U.S. companies will be better off, especially in those service industries that are relatively immune to imports.

The Chinese are pragmatic and will probably give way on issues such as intellectual property and access to markets. Xi’s China is fading, much like Japan after the late-1980s collapse in stocks and real estate.

A. Gary Shilling is president of A. Gary Shilling & Co., a New Jersey consultancy, and author of “The Age of Deleveraging: Investment Strategies for a Decade of Slow Growth and Deflation.”

No comments:

Post a Comment